Photocure Partner Asieris publishes Phase III Results from the APRICITY Study for Cevira (APL-1702) in Med journal

Asieris Pharmaceuticals (Stock Code: 688176.SH), announced today that the international multicenter phase III clinical study data of its non-surgical treatment candidate for cervical High-Grade Squamous Intraepithelial Lesion (HSIL) product APL-1702 (Cevira®) have been published online in Med, a flagship medical journal from Cell Press.

Cevira is currently undergoing regulatory review in China.

Read Asieris’ full media release here: https://asieris.com/asieris-publishes-findings-from-the-apricity-study-a-multicenter-phase-iii-global-clinical-trial-of-apl-1702-in-cell-press-journal-med/

About Cevira® (APL-1702) and Asieris

Based on the principles of photodynamic therapy, Cevira® (APL-1702) is undergoing clinical development for use as a photosensitizer in combination with light activation for the non-surgical treatment of high-grade squamous intraepithelial lesions (HSIL) in patients aged 18 years and above, excluding carcinoma in situ. Photocure developed Cevira through Phase I and Phase II clinical trials, and in July 2019, Asieris Meditech Co., Ltd licensed from Photocure the worldwide rights to develop and commercialize this drug-device combination product candidate. In November 2020, Asieris initiated a Phase III clinical trial for APL-1702 (Cevira) which achieved its primary endpoint in September 2023 (Clinical trial number: NCT04484415). The new drug application for Cevira was accepted by the National Medical Products Administration (NMPA) in May 2024, and is currently undergoing regulatory review in China.

Asieris Pharmaceuticals(688176.SH) is a global biopharmaceutical company specializing in the discovery, development, and commercialization of innovative drugs for genitourinary tumors and related diseases.

Questions about clinical development, regulatory application, or commercial strategy for APL-1702 (Cevira) should be directed to Asieris. Investors - Asieris Pharmaceuticals

2 Likes

Norsk:

Photocure-partner Asieris publiserer fase III-resultater fra APRICITY-studien for Cevira (APL-1702) i Med journal

Asieris Pharmaceuticals (aksjekode: 688176.SH) kunngjorde i dag at data fra den internasjonale multisenter kliniske fase III-studien av selskapets ikke-kirurgiske behandlingskandidat for cervikal høygradig plateepitelial lesjon (HSIL) APL-1702 (Cevira®) har blitt publisert på nett i Med, et flaggskipmedisinsk tidsskrift fra Cell Press.

Cevira gjennomgår for tiden regulatorisk vurdering i Kina.

Les hele pressemeldingen til Asieris her: https://asieris.com/asieris-publishes-findings-from-the-apricity-study-a-multicenter-phase-iii-global-clinical-trial-of-apl-1702-in-cell-press-journal-med/

Om Cevira® (APL-1702) og Asieris

Basert på prinsippene for fotodynamisk terapi, er Cevira® (APL-1702) under klinisk utvikling for bruk som fotosensibilisator i kombinasjon med lysaktivering for ikke-kirurgisk behandling av høygradige plateepiteliale intraepiteliale lesjoner (HSIL) hos pasienter i alderen 18 år og eldre, unntatt karsinom in situ. Photocure utviklet Cevira gjennom kliniske studier i fase I og fase II, og i juli 2019 lisensierte Asieris Meditech Co., Ltd fra Photocure de globale rettighetene til å utvikle og kommersialisere denne kombinasjonskandidaten for legemiddel og enhet. I november 2020 startet Asieris en klinisk fase III-studie for APL-1702 (Cevira), som oppnådde sitt primære endepunkt i september 2023 (klinisk studienummer: NCT04484415). Søknaden om det nye legemidlet for Cevira ble godkjent av National Medical Products Administration (NMPA) i mai 2024, og er for tiden under regulatorisk vurdering i Kina.

Asieris Pharmaceuticals (688176.SH) er et globalt biofarmasøytisk selskap som spesialiserer seg på oppdagelse, utvikling og kommersialisering av innovative legemidler for svulster i kjønnsorganer og relaterte sykdommer.

Spørsmål om klinisk utvikling, regulatorisk søknad eller kommersiell strategi for APL-1702 (Cevira) bør rettes til Asieris. Investorer - Asieris Pharmaceuticals

4 Likes

PHOTOCURE GOES AI

Exploration of Novel AI-enabled BlueLight Enhanced Cystoscopy (ENAiBLE)

Study Overview

Brief Summary

Blue light cystoscopy (BLC) is a diagnostic procedure in bladder cancer where the inside of the bladder is observed with a camera to detect bladder lesions. Unlike regular white lightcystoscopy, blue light cystoscopy takes use of a drug that induces fluorescence under bluelight preferentially in neoplastic and malignant cells that helps visualize bladder lesions during the cystoscopic procedure. Blue lightcystoscopy has shown to improve detection of bladder cancer. The purpose of the study is to collect images, video and associated pathology results from blue light cystoscopy procedures to explore potential of and develop an AI decision support tool. The decision support tool is hypothesized to further improve the diagnostic accuracy of the blue light procedure.

https://clinicaltrials.gov/study/NCT07144319?term=blue%20light%20cystoscopy&rank=3

Official Title

Exploration of Novel AI-enabled Blue LightEnhanced Cystoscopy

Conditions

Data Collection for AI Development

Other Study ID Numbers

- PCAIX01/25

Study Start (Estimated)

2025-09

Primary Completion (Estimated)

2026-12

4 Likes

Blue light cystoscopy (BLC) is a diagnostic procedure in bladder cancer where the inside of the bladder is observed with a camera to detect bladder lesions. Unlike regular white light cystoscopy, blue light cystoscopy takes use of a drug that induces fluorescence under blue light preferentially in neoplastic and malignant cells that helps visualize bladder lesions during the cystoscopic procedure. Blue light cystoscopy has shown to improve detection of bladder cancer. The purpose of the study is to collect images, video and associated pathology results from blue light cystoscopy procedures to explore potential of and develop an AI decision support tool. The decision support tool is hypothesized to further improve the diagnostic accuracy of the blue light procedure.

Skal kjøres på 500 pasienter.

5 Likes

Dette innlegget ble rapportert og er midlertidig skjult.

1 Like

Jeg er trolig mest blasert av AI-hypen av alle her inne, men her er det dels tvingende nødvendig at de tar eierskap for hva AI kan (eller mest sannsynlig: ikke kan) gjøre for denne typen billeddiagnostikk.

1 Like

Dette er jo for å møte konkurransen fra hvitt lys kombinert med AI og som leverer bedre resultater enn hvitt lys uten AI. Om hvitt lys med AI nærmer seg BLC uten AI kan det bli vanskelig å selge inn BLC som jo har en tyngre prosedyre enn hvitt lys. Dette ble diskutert på tråden for ett til to år siden, så det er ikke noe nytt.

AI er jo faktisk veldig bra på bildediagnostikk, noe som er etablert standard innen flere områder. For eksempel har man på enkelte sykehus i Norden erstattet den ene av de to radiologene som gransker bildene med AI siden kliniske forsøk viser at resultatene blir bedre (og man frigjør ressurser/øker kapasiteten).

Det er også gjort forsøk på AI med hvitt lys som viser gode resultater.

Nøkkelen er å ha ett kontrollert datasett av tilstrekkelig størrelse å øve AIen på. Det burde PHO ha, eller skaffe seg fra sine kunder.

3 Likes

25 Likes

11 Likes

Link nederst:

The presentation will be held in English and questions can be submitted throughout the event. The streaming event is available through: https://channel.royalcast.com/landingpage/hegnarmedia/20251029_2/

2 Likes

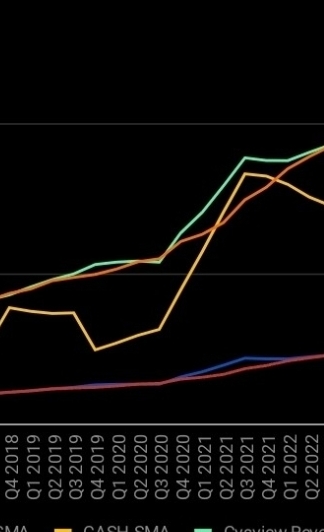

Core business på Cysview vokser, men den vokser veldig sakte.

Her er 4 kvartals glidende snitt, og sum 4 siste kvartaler. Cysview revenue trenger å stige fortere, og opex trenger å holde seg mer eller mindre flatt:

Dette var en svak G+ rapport for Q3, ikke i nærheten av noen M.

Håper de snart bruker nye 50 millioner på tilbakekjøp, ser ingen grunn til at de trenger å sitte på hundrevis av millioner.

5 Likes

Norne

Photocure delivered yet another solid quarter, with 3Q figures broadly exceeding our estimates. The company continued to post double-digit YoY growth on the top line while maintaining well-contained opex. Reported EPS came in above our expectations, and the cash position remains solid. We believe this robust financial performance further underpins our investment case on the stock going forward.

4 Likes

Hypen startet vel i 2018 hvis jeg husker rett. Siden har det gått rimelig trått

Det kan være et tidsgap mellom økt skop-portefølje og hva som resulterer i løpende salg. Med en stigning på 24% forrige Q og 23% i dette i utplasserte skop, noe som er svært positivt, mens det er en salgsøkning på 14 % på ett år bør det ligge an til en implisitt salgsøkning av Cysview fremover. Avgjørende er frekvensen i bruken. Det blir vel litt tilbakeskuende i din vurdering. Det positive nå er at Pho hele tiden bedre sine salgsbase.

ForTec has acquired and deployed 6 additional BLC towers, bringing the total number of mobile BLC towers to 24. With the increasing momentum provided by ForTec’s mobile solution, Photocure had 373 active accounts in the U.S. at the end of the quarter, an increase of 23% versus the second quarter of 2024.

Ser du på plottet egentlig? Var jo en periode rett før corona veksten var eksplosiv, så flatet det helt ut igjen. Er sånn trend de trenger igjen, uten at kostnadene stiger særlig.

2 Likes

Det kan være grunn til å legge vekt på de senere NMIBC-rapportene og at selskapet mener det vil gi vedvarende inntektsvekst.

DS skriver: Looking ahead, we anticipate sustained revenue growth, fueled by rigid kit adoption, expansion of mobile BLC, and HD upgrades that enhance utilization and sales. The tailwinds from a wave of recently approved NMIBC therapeutics are raising awareness around early detection and personalized disease management, validating Photocure’s position at the center of this rapidly evolving ecosystem.

1 Like